Please email us if you'd like a full copy of the monthly stats.

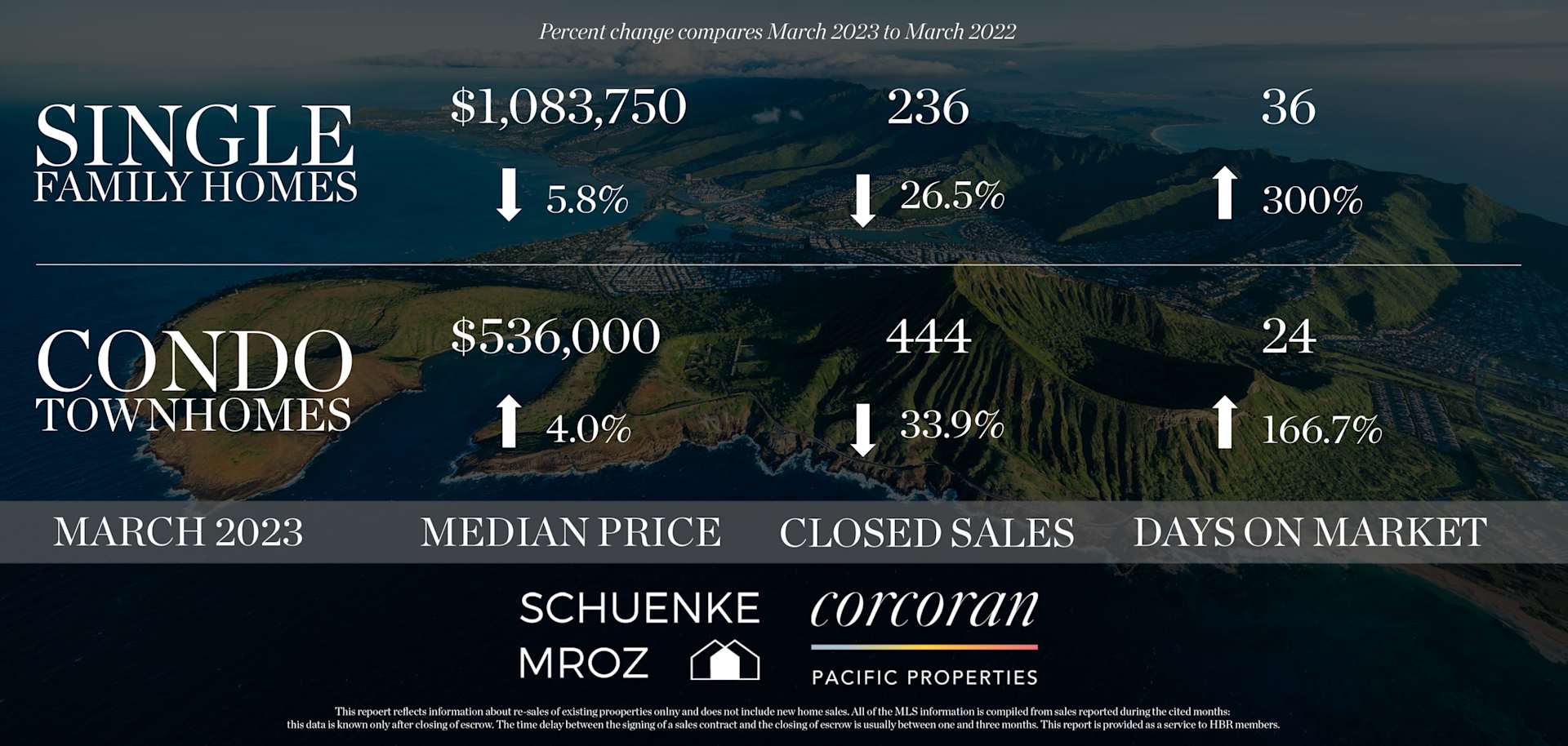

O‘ahu’s housing market experienced a boost in activity from February to March, with sales rising approximately 36% month-over-month in both single-family home and condo markets. Although year-over-year sales continued to fall short of 2022 – down 26.5% for single-family homes and 33.9% for condos year-over-year – 236 single-family homes and 444 condos sold in March 2023.

Median sales prices for March 2023 increased from January and February but were mixed compared to a year ago. The monthly median price for single-family homes declined 5.8% from $1,150,000 in March 2022 to $1,083,750 last month. Meanwhile, the condo median sales price in March set a new record of $536,000, 0.4% above the previous record of $534,000 set in June 2022, and a 4.5% rise year-over-year.

In March 2023, 58.5% of single-family home sales closed at $1,000,000 or more, pushing the median sales price above $1 million. However, the $600,000 to $799,999 price range was one of the few to see a year-over-year increase in sales volume, jumping 70.6% from 17 to 29 single-family home sales compared to the same time last year. Meanwhile, the $800,000 to $999,999 price range accounted for more than a quarter of the month’s sales.

Most single-family homes and condos continued to close for less than the original asking price. In March, approximately 35% of single-family homes closed at full asking price or more, compared to around 74% in March 2022. In the condo market, 41% of condos sold at the full asking price or more compared to 65% in March 2022.

Properties sold in March 2023 were on the market longer than those in March 2022. Median days on market for single-family homes was 36 days and for condos 24 days, compared to a 9- day median in both markets one year ago.

In the single-family home market, active inventory in the $800,000 to $899,999 range saw the most significant change, with approximately triple the number of listings at 76, compared to 25 a year ago. For condos, the increase in active inventory was mainly in the $400,000 and above range, where the number of available listings increased by 39% year-over-year.

New listing volume improved from February to March, up 25.8% month-over-month for single- family homes and 14.5% for condos. Still, new listings continued to see year-over-year declines, and the first quarter ended with total new listings down approximately 28% in both markets compared to the first quarter of 2022.

Pending sales increased from a month ago, with 258 contract signings in the single-family home market and 444 in the condo market. Compared to February, this increased by 18.9% for single-family homes and 11.3% for condos. However, pending sales volume fell short by more than 30% year-over-year in both markets.